This website and its content are not intended to provide professional or financial advice. The views expressed here are based solely on the writer’s opinion, research, and personal experience, and should not be taken as factual information. The author is not a financial advisor and lacks relevant certifications in that regard. We highly recommend consulting a qualified financial advisor before making any investment decisions, as the information presented on this site is general in nature and may not be tailored to individual needs or circumstances.

Introduction to Palantir Technologies

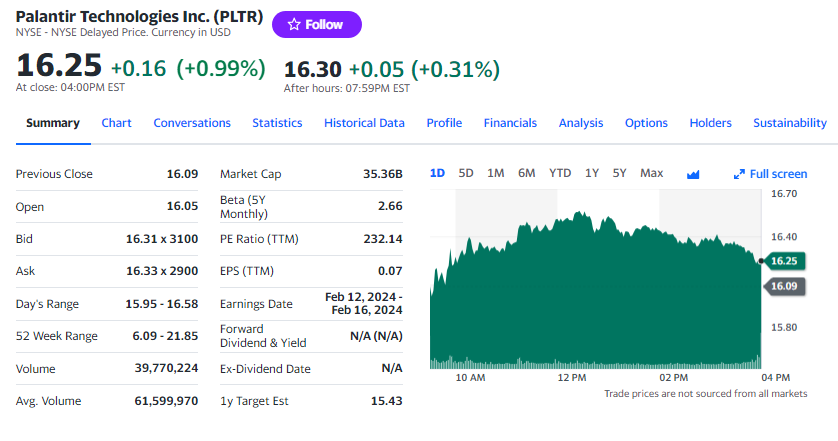

Palantir Technologies Inc., trading under the ticker PLTR on the NYSE, stands as a notable player in the realm of big data analytics. Specializing in software that assists organizations in data-driven decision-making, Palantir has carved out a significant niche in both government and commercial sectors. As of the latest market check, PLTR is valued at $16.25 per share, reflecting the dynamic nature of its market performance.

The company’s journey has been marked by a series of strategic moves and technological advancements, positioning it as a key contributor to the data analytics industry. Palantir’s software platforms, primarily known for their advanced data integration and analytical capabilities, have been instrumental in addressing complex data challenges across various domains, including defense, intelligence, and commercial enterprises.

In recent times, Palantir has continued to evolve, adapting to the changing market conditions and customer needs. The company’s ability to secure significant deals and partnerships has been a testament to its robust business model and innovative approach. This has not only bolstered its market presence but also played a crucial role in shaping its financial trajectory.

The company’s recent financial performance has drawn considerable attention from investors and market analysts alike. With a focus on expanding its client base and enhancing its technological offerings, Palantir has demonstrated a commitment to sustained growth and profitability. The company’s strategic initiatives, coupled with its strong market positioning, make it a compelling case for analysis and review.

Palantir’s Financial Performance: A Comprehensive Overview

Palantir Technologies Inc. has recently showcased a financial performance that captures the attention of both investors and industry analysts. The company’s ability to exceed expectations in its quarterly earnings reports is a testament to its robust operational strategy and market adaptability.

Earnings and Revenue Insights

In its latest financial disclosure, Palantir reported a revised earnings per share that outperformed analyst predictions. This achievement is not just a numerical victory but a strong indicator of the company’s financial health and operational efficiency. The reported revenue figures also surpassed expectations, signaling a positive trend in the company’s financial journey.

A key highlight of Palantir’s financial report is the significant growth in U.S. commercial revenue. This growth is not merely a reflection of increased sales but also an indication of the company’s expanding influence in the commercial sector. The increase in the U.S. commercial client count, from 80 to 143 over the past year, underscores Palantir’s growing appeal in the market and its ability to attract new business.

Profitability and Market Response

For the first time, Palantir reported a positive GAAP net income, marking a milestone in its journey towards sustainable profitability. This achievement is particularly noteworthy as it represents a shift from a growth-focused approach to a more balanced strategy emphasizing both growth and profitability.

The market’s response to Palantir’s financial performance has been mixed. While the stock experienced a surge following the earnings report, it also showed signs of volatility. This fluctuation can be attributed to various factors, including market sentiments and broader economic conditions.

Analyst Perspectives

The financial community’s reaction to Palantir’s performance has been varied. Some analysts have expressed concerns over the company’s top-line guidance for the upcoming quarters, suggesting a cautious approach to its future revenue projections. However, others have acknowledged the company’s better-than-expected profits, viewing it as a positive sign of its evolving business model.

Despite these differing views, there is a consensus on the potential of Palantir’s technology and its role in the data analytics sector. The company’s focus on large enterprises and government clients, though contributing to revenue volatility, is also seen as a strategic advantage that could yield long-term benefits.

Stock Performance and Market Response

Palantir Technologies Inc. has experienced a dynamic trajectory in the stock market, reflecting the evolving investor sentiment and market conditions. The company’s stock performance is a critical aspect to consider, as it offers insights into investor confidence and the perceived value of Palantir’s offerings.

Recent Stock Trends

The stock price of Palantir has seen notable fluctuations in recent times. Following the release of their positive quarterly earnings, shares soared, indicating a strong market response to the company’s financial achievements. This surge was a clear sign of investor enthusiasm and confidence in Palantir’s growth prospects.

However, the stock has also experienced periods of volatility. After the initial spike, there was a noticeable slowdown in the stock’s momentum. This pattern of rise and fall is not uncommon in the tech sector and can be attributed to various factors, including market speculations, overall economic trends, and investor reactions to company-specific news.

Impact of Leadership Statements

The company’s leadership, particularly CEO Alex Karp, has played a significant role in influencing investor perceptions. Karp’s comments regarding potential mergers and acquisitions sparked interest among investors, leading to increased speculation and activity around Palantir’s stock. Such statements from company executives often have a direct impact on stock performance, as they can signal future strategic moves and potential growth opportunities.

Year-Over-Year Analysis

Looking at Palantir’s stock performance over the past year provides a broader perspective on its market standing. Despite the recent upticks, the stock has seen a decline over the year. This decline can be viewed in the context of the company’s ongoing transition from a growth phase to a more profitability-focused approach, as well as the general market conditions affecting tech stocks.

Investor Outlook

Investors and market analysts closely monitor Palantir’s stock for indications of the company’s long-term viability and growth potential. The mixed responses – from optimism following financial reports to caution due to market volatility – reflect the complex nature of investing in technology stocks. Palantir, with its unique position in the data analytics sector, continues to be a subject of keen interest for those looking to understand the future of tech investments.

Palantir’s Revenue Growth and Future Projections

Palantir Technologies Inc.’s revenue growth and future projections are pivotal in understanding the company’s long-term potential and market position. By examining these aspects, investors and analysts can gauge the trajectory of Palantir’s business and its ability to sustain and increase its market share.

Revenue Trends and Analysis

Palantir has experienced a notable pattern in its revenue growth. While the company has consistently increased its revenue year-over-year, there has been a variation in the growth rate. In the most recent financial year, Palantir’s revenue growth was substantial, though it fell short of the company’s medium-term goal of approximately 30% annual growth. This slowdown can be attributed to various factors, including market saturation in certain segments and the natural challenges of scaling at a high rate.

Despite this, Palantir’s ability to grow its revenue in a challenging economic environment is commendable. The company’s focus on expanding its client base, especially in the U.S. commercial sector, has been a key driver of this growth. The increase in U.S. commercial revenue, which rose significantly year-over-year, is a strong indicator of Palantir’s growing market acceptance and the effectiveness of its business strategies.

Customer Engagement and Revenue Growth

An important aspect of Palantir’s revenue growth is its customer engagement. The company has not only increased its customer count but has also managed to enhance engagement with existing clients. This is evident from the higher revenue generated from long-term customers, indicating a strong and growing reliance on Palantir’s services. Such deepened engagement is crucial for sustainable growth, as it leads to more stable and predictable revenue streams.

International Market Performance

While Palantir has seen considerable success in the U.S. market, its performance in international markets has been mixed. The company faces different challenges and competition in these markets, which has affected its growth rate. However, Palantir’s continued efforts to expand its international presence and adapt its offerings to different market needs are key to its global growth strategy.

Investment Perspective: Risks and Opportunities

When evaluating Palantir Technologies Inc. from an investment standpoint, it’s essential to weigh both the potential risks and opportunities that the company presents. This balanced view helps investors make informed decisions based on the company’s current performance and future prospects.

Potential Investment Risks

- Market Volatility: Palantir’s stock has shown volatility, which could be a concern for risk-averse investors.

- Dependence on Government Contracts: A significant portion of Palantir’s revenue comes from government contracts, making it susceptible to changes in government spending and policy.

- Competitive Industry: The data analytics sector is highly competitive, with constant technological advancements. Keeping pace with these changes is crucial for Palantir’s sustained success.

- Global Expansion Challenges: As Palantir expands internationally, it faces challenges in adapting to different market dynamics and regulatory environments.

Opportunities for Growth

- Expanding Commercial Sector: Palantir’s growing presence in the commercial sector diversifies its revenue streams and reduces reliance on government contracts.

- Innovative Solutions: The company’s continuous innovation in data analytics positions it to capitalize on the growing demand for advanced data solutions.

- Strategic Partnerships: Collaborations with other tech leaders can open new markets and enhance Palantir’s offerings.

- Long-term Government Relationships: Palantir’s established relationships with government agencies provide a stable revenue base and opportunities for new contracts.

FAQs

Palantir specializes in creating advanced data analytics software. Their platforms are designed for integrating, managing, and analyzing large datasets, primarily serving government agencies and large enterprises.

Palantir generates revenue primarily through its government and commercial contracts. The company offers data analytics services to government agencies for national security and defense purposes, as well as to commercial enterprises for data-driven decision-making.

Investing in Palantir involves risks like market volatility, dependence on government contracts, intense competition in the data analytics sector, and challenges in global expansion.

The future outlook for Palantir is focused on expanding its commercial sector presence, penetrating global markets, and continuing technological innovation. While facing challenges such as market volatility and competition, these strategic initiatives are expected to drive the company’s growth.

Conclusion

In conclusion, Palantir Technologies Inc. stands as a resilient and adaptive force in the data analytics sector, marked by its ability to surpass financial expectations and innovate continuously. While facing challenges such as market volatility and intense competition, Palantir’s strategic expansion into the commercial sector and global markets, coupled with its commitment to technological advancement, positions it for potential growth. Investors and market observers will find Palantir’s journey a compelling blend of opportunities and challenges, making it a noteworthy entity in the evolving landscape of technology and data analytics.

StockHax strives to provide unbiased and reliable information on cryptocurrency, finance, trading, and stocks. However, we cannot provide financial advice and urge users to do their own research and due diligence.

Read More

{kind=link}