{kind=link}

This website and its content are not intended to provide professional or financial advice. The views expressed here are based solely on the writer’s opinion, research, and personal experience, and should not be taken as factual information. The author is not a financial advisor and lacks relevant certifications in that regard. We highly recommend consulting a qualified financial advisor before making any investment decisions, as the information presented on this site is general in nature and may not be tailored to individual needs or circumstances.

Your stock trading experience essentially boils down to two choices: Do you want automated, affordable trades or a slightly more boutique, human-led experience? To answer that question, we’re going to rate the advantages and disadvantages of personal advisor service Vanguard and robo-trader Fidelity to see which one wins out.

Contents

Features, Fees & Ratings Comparison Table

| Features | Vanguard | Fidelity |

|---|---|---|

| 💰 Account Minimum | $0 for most accounts | $0 for brokerage accounts and $2,500 for managed accounts |

| 💸 Commission Fees | $0 commission for online trades of Vanguard ETFs® and other ETFs. $0 commission for online trades of stocks (excluding penny stocks). $1 per contract for online trades of options (subject to a $10 minimum per trade). $0 commission for online trades of mutual funds from other companies (excluding certain fund families). Fees vary for other types of mutual funds and brokered CDs. | $0 for stocks, ETFs, and options trades. $0.65 per options contract. Mutual funds have $49.95 transaction fees. |

| 💼 Investment Options | Stocks, ETFs, mutual funds, bonds, CDs, options, and more. | Stocks, bonds, ETFs, mutual funds, options, and CDs |

| 🤖 Robo-Advisor | Vanguard Digital Advisor: Automated investment management service | Fidelity Go, which charges a 0.35% annual advisory fee and has a $10 minimum investment |

| 📊 Research and Analysis | Yes, Vanguard offers various research and analysis tools such as market insights, fund screeners, portfolio analysis, and more. | Extensive research and analysis tools, including reports, screeners, and educational content |

| 📱 Mobile App | Yes, Vanguard has a mobile app that allows you to access your account, trade investments, check balances, review performance, and more. | Fidelity Mobile App |

| 🏦 Retirement Accounts | Yes, Vanguard offers various retirement accounts such as traditional IRA, Roth IRA, SEP-IRA, SIMPLE IRA, individual 401(k), and rollover IRA. | Traditional and Roth IRAs, SEP IRAs, SIMPLE IRAs, and 401(k) plans |

| 📈 Trading Platform | Yes, Vanguard has a trading platform that allows you to buy and sell investments online with ease and convenience. | Fidelity offers a web-based trading platform and the Active Trader Pro desktop platform for frequent traders |

| 📞 Customer Service | Yes, Vanguard has a customer service team that is available to assist you with your account and investment needs. | 24/7 phone support and online chat. Over 190 branch locations for in-person support |

| 📚 Educational Resources | Yes, Vanguard offers various educational resources such as articles, videos, podcasts, webinars, calculators, and more to help you learn about investing and improve your financial literacy. | Extensive educational resources, including articles, videos, webinars, and courses |

| 🌕 Fractional Shares | No, Vanguard does not offer fractional shares trading at this time. | Yes, through Fidelity’s mobile app and website |

| 🌱 Socially Responsible | Yes, Vanguard offers socially responsible investing options such as ESG (environmental, social, and governance) funds that seek to align your investments with your values and beliefs. | Offers ESG-focused funds and tools for socially responsible investing |

| 🌎 International Investing | Yes, Vanguard offers international investing options such as global and international funds that allow you to diversify your portfolio across different countries and regions. | No |

| 💳 Cash Management | Yes, Vanguard offers cash management services such as a settlement fund that acts as a holding place for money waiting to be invested or withdrawn from your account. | Fidelity Cash Management account offers FDIC-insured checking and ATM fee reimbursements |

| 🔍 Margin Trading | Yes, Vanguard offers margin trading services that allow you to borrow money from your brokerage account to buy securities on credit. | Yes, with competitive rates |

| ⚙️ Options Trading | Yes, Vanguard offers options trading services that allow you to buy or sell contracts that give you the right to buy or sell an underlying asset at a specific price within a specific time period. | Extensive options trading tools and resources |

| ₿ Cryptocurrency Trading | Does not offer cryptocurrency trading | No |

| 🛡️ Account Security | Uses industry-standard security measures, including two-factor authentication | Two-factor authentication and advanced encryption technologies |

| 💹 Leverage | Offers margin trading with leverage | No |

| ⚖ Regulation | Regulated by the U.S. Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) | Fidelity is regulated by the SEC and FINRA in the US, and the FCA in the UK. It is also a member of SIPC. |

Vanguard vs. Fidelity

In the world of brokerage firms, Vanguard and Fidelity are two of the most respected and well-established names. Both companies offer a wide range of investment products and services, catering to individual investors with varying preferences and financial goals. As you compare Vanguard and Fidelity, it’s essential to consider factors such as investment options, fees, trading platforms, and customer service to determine which brokerage firm best aligns with your needs. In this comparison of Vanguard vs. Fidelity, we’ll explore the unique features and benefits of each company, helping you make an informed decision about which one is right for your investment journey.

Vanguard

Vanguard is a renowned investment management company with a long-standing reputation for low-cost, passive investment strategies. Established in 1975 by John C. Bogle, the company has grown to become one of the largest and most respected brokerage firms in the world. With a focus on providing individual investors access to a wide range of low-cost index funds and ETFs, Vanguard has built its brand on the foundation of helping everyday investors achieve their financial goals.

- Low-cost investment options

- Strong reputation

- Wide range of investment options

- Focus on long-term investing

- Limited trading tools and research

- No commission-free individual stock trading

- Customer service

Vanguard is a suitable choice for investors seeking low-cost, passive investment options with a long-term focus. Its strong reputation and wide range of investment products make it a popular choice for many individual investors. However, if you’re looking for advanced trading tools or commission-free stock trading, you may want to consider Fidelity as an alternative.

Fidelity

Fidelity is a well-established financial services company founded in 1946, offering a comprehensive suite of investment products and services. Known for its wide range of investment options, including mutual funds, ETFs, stocks, and bonds, Fidelity has earned a reputation for providing individual investors with the tools, resources, and support they need to manage their portfolios effectively. With an extensive suite of trading tools and research capabilities, Fidelity caters to investors of all experience levels, from beginners to seasoned professionals.

- Commission-free trading

- Robust trading platform

- Wide range of investment options

- Excellent customer service

- Higher fees on some mutual funds

- Limited access to low-cost index funds

Fidelity meets the criteria for investors seeking a robust trading platform, commission-free trading, and responsive customer service. Its wide range of investment products and resources cater to investors of all experience levels. However, for those specifically focused on low-cost index funds, Vanguard may be a more suitable choice due to its larger selection and emphasis on passive investing.

Features & Primary Uses

Vanguard and Fidelity control and manage more than $5 trillion in assets between them, which makes them two of the biggest names in money management. And both companies have a serious set of features that appeal to many investors.

Both Fidelity and Vanguard specialize primarily in index funds — the low-cost, diversified funds that lower risk and offer some of the most stable, consistent returns on investment. While Vanguard is the innovator of the index fund (the Vanguard 500 Index Fund is commonly considered the very first of its kind), Fidelity recently started providing index funds that are just as affordable.

In addition to index funds, Fidelity works with active and passive funds, so it has a leg up in terms of variety; Vanguard works mostly with the aforementioned index funds. However, Vanguard’s vast selection of index funds give you plenty of options if that’s the route you are looking to take.

For traders, there are online platforms for both companies so you can track your account progress. However, given Vanguard’s greater dedication to passive, hands-off, advisor-based trading, their platform feels a little old when compared to the comprehensive, features-heavy nature of Fidelity’s software. Then again, Vanguard specializes in passive investment funds that track the markets, so investors can gauge how their funds are performing by watching the financial markets.

One of the most innovative aspects of Vanguard is that it is structured to make the shareholders of the funds it manages the owners of the company itself. This cuts out the middle man, and allows the firm to pass along cost savings to customers/shareholders.

Fidelity, meanwhile, is more concerned with active wealth management, and maintains its affordability and popularity through an impressive array of financial advisory services, asset management tools and online tools. This makes it perfect for more hands-on investors, as it allows them to put in the work themselves, saving a little money in the process and getting more control over their investments.

Fidelity is the bigger investment firm, which brings with it a certain level of credibility — going with them means having the security of working with one of the largest and most reputable investment companies around. This means that Fidelity traders often have great access to competitive IPOs and private placements, which is certainly a boon.

The Vanguard group is no small potatoes, though; they’re the largest mutual fund company in the world, and their commitment to index funds has allowed them to remain the top name in that particular field of investment. By having sub-advisors manage your investments, there is less of a chance of portfolio inbreeding, which is certainly advantageous and sidesteps the problems that come with that strategy.

Investment Options

Both Fidelity and Vanguard provide a variety of reputable investment options, though their focuses are somewhat dissimilar. Vanguard, for instance, mostly works in ETFs and mutual funds, often classified by share class. You can allocate them in either taxable accounts or IRAs of all kinds.

Fidelity allows for a much wider variety of options, however, trading in a number of low-cost stocks, ETFs, mutual funds, options, CDs, and international investments. You can even trade in precious metals. All of these run at the same $7.95 equity trade rate, with unlimited shares and unlimited trades for all customers.

From a variety perspective, Fidelity wins out — their ability to trade internationally is a huge boon, as is their focus on many different kinds of investments and a more active trading philosophy. Most trades are made with the Fidelity Contrafund, a diversified fund that invests in companies thought to have multi-year growth, even if the current prices don’t reflect that.

Fees

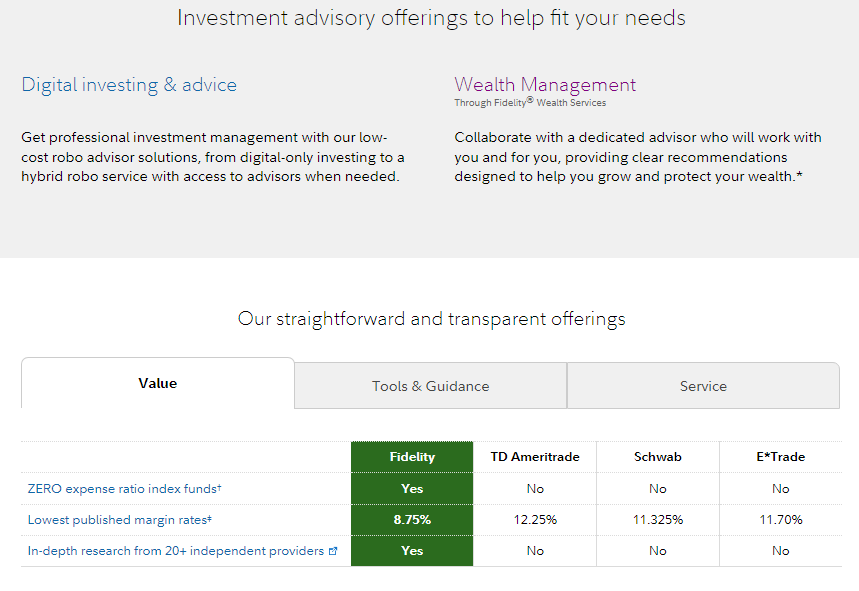

The overall costs of Fidelity and Vanguard vary quite a bit based on what you’re looking for. On the whole, Fidelity is the much better entry-level solution — there is a $2,500 minimum balance required, and it only costs $7.95 per trade to work on your investments.

Fidelity’s low trade rate is one of its biggest selling points — for a hands-on, automated online broker, there are only a few places that have such a low price per trade. It can add up over time, but there are investment strategies where that rate would be tough to beat.

Vanguard, on the other hand, requires a minimum of $50,000 in order to qualify for their personal advisor service, which is the real reason you would want to go with them in the first place.

Overall, Vanguard has the higher incentive to provide lower rates to its customers, as they are the co-owners of the company — they have a motto that their funds own the company and investors own the funds.

Vanguard Regulations

In the USA, Vanguard Group Inc is a registered investment advisor with SEC and it also offers mutual funds and ETFs that are subject to various tax rules and regulations. Vanguard Marketing Corporation is an investment adviser registered with SEC and it also acts as a distributor for Vanguard funds. Vanguard Brokerage Services is a division of Vanguard Marketing Corporation that provides brokerage services to clients and is regulated by FINRA (treasury.gov.au).

• In the UK, Vanguard Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) and is authorised to passport its investment services and activities into other EU countries (treasury.gov.au). It offers various funds and ETFs to UK investors. Vanguard Investments UK Limited is an intermediary subsidiary of Vanguard Group Inc that provides marketing services for Vanguard Asset Management Limited.

• In Australia, Vanguard Investments Australia Ltd (VIA) is licensed by ASIC as an Australian Financial Services Licensee (AFSL) No. 227263. It offers various funds and ETFs to Australian investors. VIA also has an Investment Stewardship team that engages with companies on environmental, social and governance (ESG) issues and discloses its voting records on its website.

Asset Allocation

In a very real way, Vanguard offers more expertly handled asset allocation, given the human element of its personal advisor service. Instead of trusting n platform, teams of advisors keep an eye on your account and make changes and adjustments in response to changing market conditions.

Central to Vanguard’s asset allocation are their portfolio allocation models, which provide a plethora of solutions to traders who either want to expand their investments, focus on fixed-income, or keep a balance between the two.

That said, Fidelity’s asset allocation is also great. Focusing heavily on diversification, Fidelity offers quite a few asset allocation funds, backed by research and providing flexibility to all their traders.

According to Fidelity themselves, they perform fundamental, quantitative, and macroeconomic analysis for all funds and portfolios in order to find the best investment ideas to fulfill their investor’s goals.

Which Should You Pick? Who Is Each Good For?

Judging the relative merits of both Vanguard and Fidelity, each seems to be good for different types of traders. Depending on the needs of the investor in question, it might be easy to choose between the two.

If your trading style is a bit more aggressive, you’ll want to go with Fidelity — the low trade cost and its online trading platform favors traders who are more hands-on. Actively managed funds are the service’s bread and butter, and over the last 10 years they’ve averaged an 8.40% ROI for investors as a result.

Fidelity’s service-oriented approach makes it easy for more technologically savvy investors to harness all the tools and features that the platform has to offer. Fidelity focuses much more on its apps and trading platforms, putting the brokerage decisions directly in the client’s hands. The research capabilities of Fidelity’s interface alone make it more attractive to active investors.

Traders who wish to be more conservative, however, might want to go with Vanguard. Most of the service’s mutual funds are index-based, which means they are not quite as actively managed by their advisors as you might think. If you want a slow, steady set of dividends that you can let others handle for you, Vanguard is your best option.

Investors looking for the best bargain might actually want to go with Vanguard, despite Fidelity’s remarkably low trade prices. Their index-based funds do not cost much — for instance, the Vanguard 500 Index Fund has only a .05% expense ratio. You can save a bit more this way than you would by relying on Fidelity’s $7.95 trades.

In the end, both Vanguard and Fidelity have incredibly strong virtues, depending on what you’re looking for. Those who want the human touch with their investments should stick with Vanguard, while more hands-on traders looking for short-term savings would do well to go with Fidelity.

Conclusion

When comparing Vanguard and Fidelity, both brokerage firms have their unique advantages and disadvantages. Vanguard stands out for its low-cost index funds and ETFs, along with its focus on long-term investing. On the other hand, Fidelity offers commission-free trading, a robust trading platform, and exceptional customer service.

Your choice between Vanguard and Fidelity will ultimately depend on your individual investment preferences and goals. If you prioritize low-cost, passive investing and are willing to forego advanced trading tools, Vanguard might better fit your needs. However, if you seek a comprehensive trading platform, commission-free trading, and a wider array of investment options, Fidelity may be the more suitable option.

StockHax strives to provide unbiased and reliable information on cryptocurrency, finance, trading, and stocks. However, we cannot provide financial advice and urge users to do their own research and due diligence.

Read More