This website and its content are not intended to provide professional or financial advice. The views expressed here are based solely on the writer’s opinion, research, and personal experience, and should not be taken as factual information. The author is not a financial advisor and lacks relevant certifications in that regard. We highly recommend consulting a qualified financial advisor before making any investment decisions, as the information presented on this site is general in nature and may not be tailored to individual needs or circumstances.

Introduction to NVIDIA’s Market Position

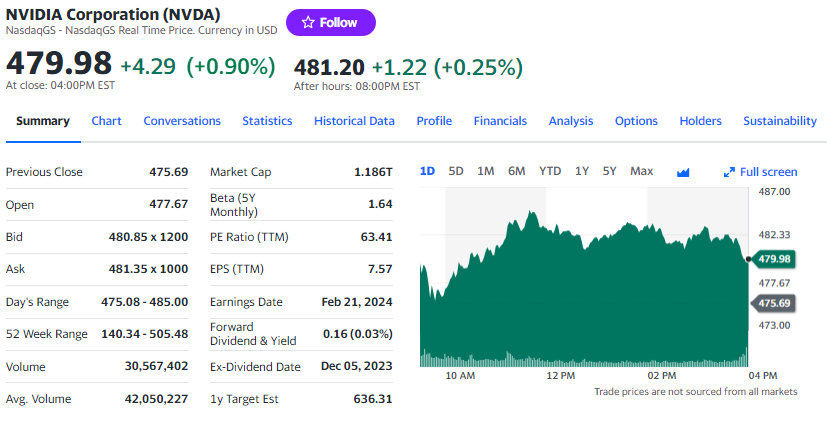

NVIDIA Corporation (NVDA), a renowned leader in the field of technology and artificial intelligence, has been a topic of keen interest for investors and market analysts alike. As of the latest update, NVIDIA’s stock stands at $479.98 on the NasdaqGS. This figure not only represents the real-time pulse of the market but also serves as a starting point for understanding the company’s current financial health and future prospects.

NVIDIA has carved out a formidable position in the tech industry, particularly in the realms of AI and gaming. The company’s innovative approach to developing advanced graphics processing units (GPUs) and AI technology has set it apart from its competitors. NVIDIA’s products are not just pivotal in gaming but also play a crucial role in areas like data centers, professional visualization, and autonomous vehicles.

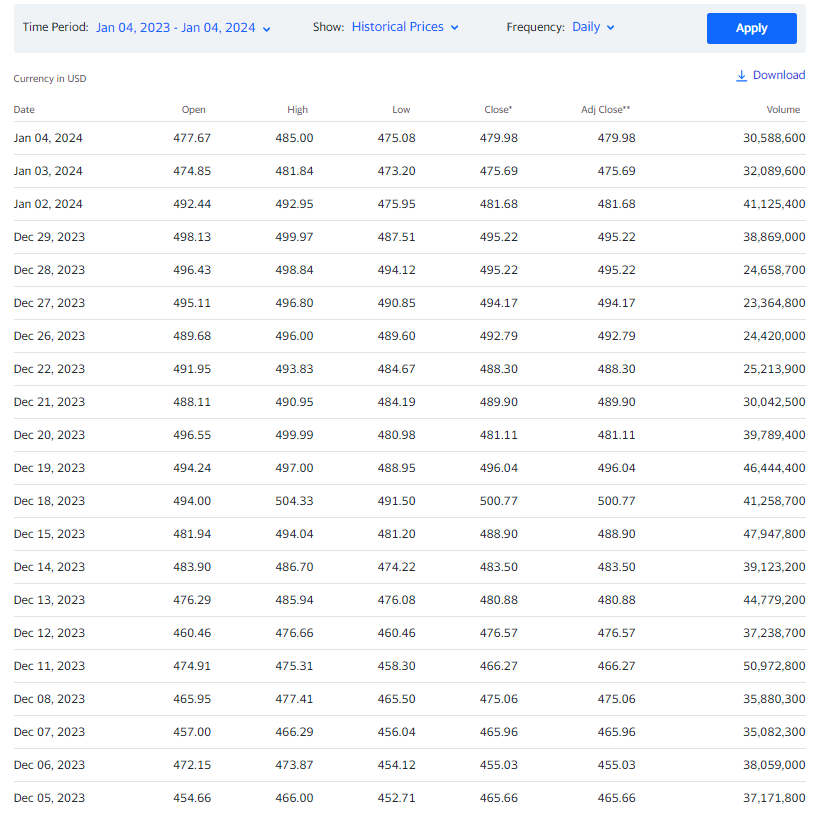

The year 2023 was a significant period for NVIDIA, marked by both challenges and achievements. Despite facing a volatile tech market and various external economic pressures, the company managed to showcase resilience. The fluctuating stock prices throughout the year reflected the dynamic nature of the tech industry, as well as NVIDIA’s ability to adapt and evolve in response to changing market conditions.

Entering 2024, NVIDIA appears poised to capitalize on the burgeoning AI sector, with its GPUs being central to the growth and development of this revolutionary technology. The company’s strategic focus on AI and deep learning has not only fortified its market position but also opened new avenues for growth. With the AI revolution gaining momentum, NVIDIA’s role as a key player in this transformation becomes increasingly vital.

Investors and market analysts are closely monitoring NVIDIA’s financial metrics, such as earnings per share (EPS), revenue growth, and forward earnings estimates. These indicators are essential for understanding the company’s performance and gauging its future potential. As the tech world continues to evolve at a rapid pace, NVIDIA’s financial health and strategic direction will be crucial factors in determining its market position and stock performance in 2024.

2023 Performance Review and 2024 Projections

In 2023, NVIDIA’s journey in the stock market was a blend of highs and lows. The company’s stock experienced significant volatility, a common phenomenon in the tech industry. This fluctuation was a response to various external economic conditions and internal industry shifts. Despite these ups and downs, NVIDIA managed to sustain a strong market presence, thanks to its continuous innovation and strategic focus.

Key Financial Metrics in 2023

Throughout the year, the company’s financial health was closely monitored, with particular attention to earnings per share (EPS) and revenue growth. These metrics were crucial in understanding NVIDIA’s operational efficiency and market positioning amidst challenging economic conditions.

Projections for NVIDIA in 2024

As we look towards 2024, analysts’ projections for NVIDIA are highly optimistic. The company’s deep involvement in the AI sector is expected to drive significant growth. NVIDIA’s GPUs, essential for AI development, are predicted to be a major factor in this upward trajectory.

Strategic Positioning and Market Dynamics

The anticipation for 2024 is also rooted in NVIDIA’s strategic positioning within the tech industry. The company’s focus on AI and deep learning technologies places it at the center of a major technological shift. With AI applications expanding, NVIDIA’s role as a crucial technology provider is expected to boost its market performance.

Key Financial Metrics and Earnings Analysis

NVIDIA’s Financial Health

NVIDIA’s financial health can be assessed through various key metrics that provide insights into its performance and market position. These metrics include earnings per share (EPS), revenue growth, and other significant financial indicators. Analyzing these will offer a clearer picture of the company’s operational efficiency and profitability.

Earnings Per Share (EPS)

Earnings per share is a crucial indicator of a company’s profitability. It represents the portion of a company’s profit allocated to each outstanding share of common stock, serving as an indicator of the company’s financial health. For NVIDIA, tracking the EPS over time helps investors understand how profitable the company is on a per-share basis.

Revenue growth is another essential metric, indicating the rate at which NVIDIA’s income is increasing over time. This growth is a vital sign of the company’s expanding business activities and market reach. It also reflects the company’s ability to sell its products and services successfully.

Forward earnings estimates are predictions about future earnings, which are important for understanding how the market perceives NVIDIA’s future performance. These estimates are based on projections made by analysts and provide insights into the expected financial trajectory of the company.

The AI Revolution and NVIDIA’s Role

NVIDIA has emerged as a dominant force in the rapidly evolving landscape of artificial intelligence (AI). The company’s advanced graphics processing units (GPUs) are at the heart of this transformation, playing a crucial role beyond the realms of gaming. These GPUs are indispensable in processing the intricate computations required for AI and deep learning, making NVIDIA a key player in the AI revolution. This technological prowess has opened doors to diverse applications, stretching from healthcare diagnostics to the intricacies of autonomous vehicles.

The strategic direction NVIDIA has taken in AI is marked by significant research and development investments, alongside collaborations across various sectors. This focus is not just about advancing AI technology but also ensuring that NVIDIA’s offerings remain essential and cutting-edge. Looking forward, NVIDIA’s influence in the AI space is only expected to grow. As AI becomes more embedded in our daily lives and its applications expand, the demand for NVIDIA’s GPUs and AI solutions is set to rise. This growth trajectory positions NVIDIA not just as a technology leader but also as a pivotal contributor to the future of AI, promising a significant impact on the company’s market position and financial performance.

Investor Sentiments and Market Predictions

Investor sentiment towards NVIDIA has been a vital factor in shaping its stock performance. In 2023, despite market volatilities, NVIDIA managed to retain investor confidence, primarily due to its strong market position and innovative edge in AI and technology. The company’s ability to navigate through economic uncertainties and maintain a steady pace of growth has been key in securing investor trust.

Market predictions for NVIDIA in 2024 are largely positive, reflecting the company’s robust standing in the tech industry. Analysts are particularly optimistic about NVIDIA’s continued leadership in AI and its potential to capitalize on this rapidly growing sector. The general consensus among experts suggests a bullish outlook for NVIDIA’s stock, driven by its strategic focus on AI and its role in the ongoing technological revolution.

These optimistic predictions are also backed by NVIDIA’s solid financial performance and its track record of innovation. The company’s financial health, as indicated by key metrics such as EPS and revenue growth, reinforces the positive sentiment among investors. Moreover, NVIDIA’s strategic investments in AI and its continuous product innovation are seen as critical factors in driving its future growth and market success.

Comparative Market Analysis

NVIDIA’s market performance can be better understood through a comparative analysis with its competitors and broader market benchmarks. This comparison provides insights into NVIDIA’s competitive advantage and its position in the tech industry.

NVIDIA vs. Competitors

When compared with its direct competitors in the GPU and AI technology sectors, NVIDIA often stands out for its innovation and market share. The company has maintained a leading position in GPU technology, primarily due to its continuous innovation and strong product offerings. However, it faces stiff competition from other tech giants who are also vying for a share of the lucrative AI and tech markets.

Market Benchmarks

Comparing NVIDIA’s stock performance with market benchmarks such as the NASDAQ or S&P 500 provides a broader view of its standing in the overall tech sector. Historically, NVIDIA’s stock has shown a strong correlation with tech industry trends, often outperforming the market during periods of technological growth and facing challenges during market downturns.

Impact of Industry Trends on NVIDIA

Industry trends, such as the growth of AI, the increasing demand for high-performance computing, and the expansion of cloud computing, have a significant impact on NVIDIA’s market position. The company’s ability to align its products and strategies with these trends is critical for maintaining its competitive edge.

Risks and Opportunities for NVIDIA in 2024

As NVIDIA navigates through 2024, it faces a mix of risks and opportunities that could impact its stock performance and market position.

Potential Risks

- Market Competition: NVIDIA operates in a highly competitive sector, facing strong rivals in both the GPU and AI markets. These competitors are constantly innovating, posing a continual challenge to NVIDIA’s market share and revenue growth.

- Economic Conditions: Global economic fluctuations, including changes in consumer spending, inflation rates, and trade policies, could influence NVIDIA’s performance. Particularly, any downturn in the tech sector could adversely affect the company’s stock.

- Technological Shifts: Rapid changes in technology can render existing products obsolete. NVIDIA must continually innovate to stay ahead, with any failure to adapt quickly posing a significant risk.

- Regulatory Challenges: Changes in regulations, especially those related to data privacy, AI ethics, and international trade, could impact NVIDIA’s operations and profitability.

Opportunities for Growth

- AI and Deep Learning: As a leader in AI technology, NVIDIA is well-positioned to capitalize on the growth of AI and deep learning applications across various industries.

- Expansion into New Markets: NVIDIA has opportunities to expand into new markets, such as healthcare, automotive, and more, leveraging its AI and GPU technologies.

- Strategic Partnerships: Collaborations with other tech giants and industry leaders could open new avenues for growth and innovation.

- Product Diversification: By diversifying its product portfolio to include not just hardware but also software and full AI systems, NVIDIA can capture a larger market share and increase its revenue streams.

FAQs

NVIDIA is primarily known for its cutting-edge graphics processing units (GPUs) used in gaming and professional markets. They have also gained significant recognition for their role in advancing artificial intelligence (AI) technology.

NVIDIA has played a crucial role in the AI industry, mainly through its GPUs which are essential for AI and deep learning applications. Their technology has enabled significant advancements in various fields, including autonomous vehicles, healthcare, and finance.

Analysts predict a bullish outlook for NVIDIA in 2024, largely driven by its leadership in AI and GPU technology. The expansion of AI applications across different sectors is expected to fuel further growth for the company.

NVIDIA faces challenges like intense market competition, rapid technological changes, and global economic fluctuations. Regulatory changes, particularly in areas like AI ethics and data privacy, also pose potential challenges.

Conclusion: Future Outlook of NVIDIA

In summary, NVIDIA’s journey through 2024 highlights its resilience and adaptability in the ever-evolving tech industry. The company’s commitment to innovation, particularly in AI and GPU technology, positions it strongly for future growth. Navigating a balance between market risks and opportunities, NVIDIA is poised to continue its leadership in the tech sector. The focus for investors and analysts will be on the company’s financial performance and strategic decisions in response to industry trends. NVIDIA’s ability to maintain investor confidence and meet market expectations will be crucial in shaping its continued success in the tech landscape.

StockHax strives to provide unbiased and reliable information on cryptocurrency, finance, trading, and stocks. However, we cannot provide financial advice and urge users to do their own research and due diligence.

Read More

{kind=link}