2024 stock performance, analyst insights, and future growth potential in our detailed analysis.){kind=link}

This website and its content are not intended to provide professional or financial advice. The views expressed here are based solely on the writer’s opinion, research, and personal experience, and should not be taken as factual information. The author is not a financial advisor and lacks relevant certifications in that regard. We highly recommend consulting a qualified financial advisor before making any investment decisions, as the information presented on this site is general in nature and may not be tailored to individual needs or circumstances.

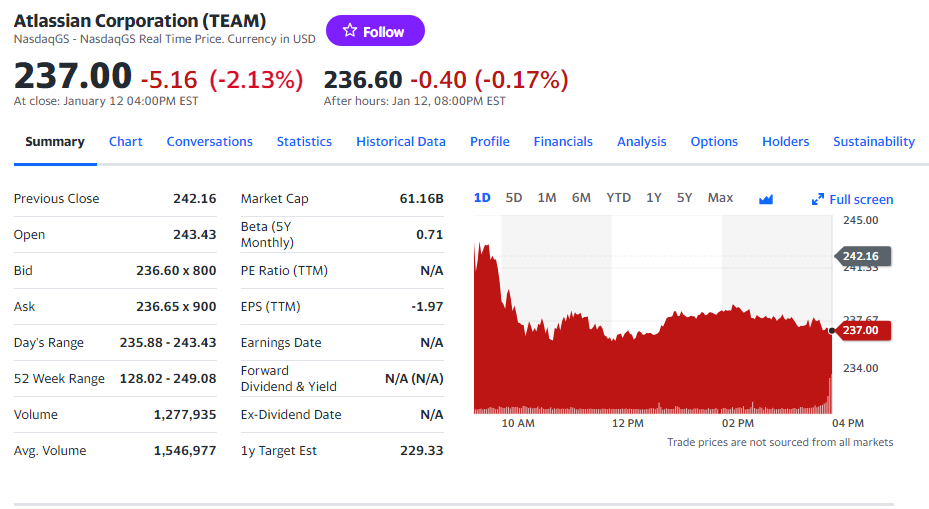

Atlassian Corporation, known for its innovative software solutions that enhance team collaboration and productivity, has consistently made headlines in the tech industry. As of January 2024, Atlassian’s (TEAM) stock price stands at $237.00, reflecting the dynamic nature of the tech market and the company’s evolving role within it.

Atlassian’s Performance Analysis: A 2024 Snapshot

The beginning of 2024 paints an intriguing picture for Atlassian. The company’s stock, trading at $237.00, demonstrates the resilience and potential growth that Atlassian embodies in the competitive software market. This valuation is a critical indicator of the company’s market position and investor confidence, considering the ebb and flow of the tech sector.

Key Financial Indicators

Atlassian’s current market capitalization, a significant measure of the company’s overall value, stands at a robust $61.16 billion. This figure is not just a testament to its current worth but also a beacon indicating its potential for future growth. Additionally, the absence of a dividend yield points to Atlassian’s strategy of reinvesting profits back into the company, a common approach among growth-oriented tech firms.

The Tech Sector’s Influence on Atlassian

The tech sector’s volatility is well-known, with rapid innovation and changing market trends constantly reshaping the landscape. Atlassian, nestled within this dynamic environment, has shown a remarkable ability to adapt and thrive. The stock’s fluctuation over the past year, ranging from a low of $128.02 to a high of $249.08, underscores the company’s resilience amidst these market shifts.

Investor Confidence and Market Dynamics

Investor sentiment towards Atlassian is a crucial element in understanding its stock performance. The company’s ability to navigate the complexities of the tech market while maintaining a strong product portfolio has kept investor confidence steady. This confidence is further reflected in the modest short interest ratio of 1.57%, indicating a generally positive market outlook for Atlassian’s shares.

Forward-Looking Perspectives

As we progress through 2024, Atlassian’s strategic initiatives and market adaptations will be key areas to monitor. The company’s positioning within the tech sector, combined with its financial indicators and investor sentiments, paints a picture of a firm poised for continued relevance and growth in a rapidly evolving industry.

Contents

Analyst Insights and Stock Forecasts for 2024

As we turn our focus to the expert analysis and forecasts for Atlassian in 2024, the overall sentiment from analysts is cautiously optimistic. The consensus among market experts is a “Moderate Buy” rating for Atlassian’s stock. This sentiment is anchored in the company’s consistent performance and its strategic positioning in the software industry.

Understanding the Consensus Rating

The “Moderate Buy” rating is derived from a comprehensive analysis of various market factors and individual analyst opinions. It represents a balanced view, acknowledging Atlassian’s potential for growth while considering the inherent uncertainties in the tech sector. This rating is based on the collective insights from 19 analysts, reflecting a broad spectrum of market perspectives.

Projected Stock Price Movements

For 2024, the analysts have set a consensus price target of $203.22 for Atlassian’s stock. This target suggests a potential downside of approximately 14.25% from the current price of $237.00. The projection is grounded in both the historical performance of the stock and the anticipated market conditions. It’s important to note that these forecasts are subject to change based on emerging market trends and company performance.

Month-by-Month Price Predictions

Analysts have also provided month-by-month price predictions for Atlassian’s stock throughout 2024. These projections offer a glimpse into the expected short-term fluctuations in the stock price, influenced by market dynamics and company-specific developments. The month-wise forecast shows variations, with certain months anticipating higher prices due to expected positive developments or market trends.

The Significance of These Forecasts

These forecasts play a crucial role for investors, providing a roadmap of what to expect in the coming months. They offer insights into the potential high and low points of Atlassian’s stock, allowing investors to plan their strategies accordingly. However, it’s essential to approach these forecasts with an understanding of their speculative nature and the unpredictable elements of the market.

The analysis and forecasts for Atlassian in 2024 paint a picture of a company with a solid foundation, poised for potential growth, yet facing the typical uncertainties of the tech sector. These insights offer valuable guidance for investors looking to make informed decisions about their investment in Atlassian.

MarketBeat’s View on Atlassian: A Deep Dive

MarketBeat, a well-regarded financial analysis and news platform, offers a nuanced perspective on Atlassian’s stock. Their insights are crucial for investors seeking a well-rounded understanding of the company’s stock potential in 2024.

Analyzing MarketBeat’s Ratings and Insights

MarketBeat assigns Atlassian a “Moderate Buy” rating, consistent with the broader analyst consensus. This rating reflects MarketBeat’s assessment of various factors, including past performance, future projections, and overall market conditions. Atlassian’s rating score of 2.53 out of 5, based on 10 buy ratings and 9 hold ratings, indicates a tempered optimism about the company’s stock performance.

MarketBeat’s Price Target for Atlassian

Further emphasizing their cautious stance, MarketBeat sets a price target of $203.22 for Atlassian’s stock. This target suggests a potential downside compared to the current trading price. This valuation is based on a detailed analysis of market trends, company performance, and sector movements.

Short Interest and Investor Sentiments

MarketBeat also reports on short interest and investor sentiments toward Atlassian. A short interest of 1.57% of outstanding shares suggests a generally positive sentiment in the market, indicating that a limited number of investors are betting against the stock. This metric is a vital indicator of market confidence in Atlassian’s future prospects.

Atlassian’s MarketRank and Sector Position

MarketBeat ranks Atlassian within its sector and industry, providing investors with a broader context of how the company stacks up against its peers. In the competitive prepackaged software industry, Atlassian’s position is noteworthy, offering insights into its market strength and potential for growth.

MarketBeat’s analysis of Atlassian underscores the company’s solid standing in the market. Their insights are integral for investors looking to gain a comprehensive view of Atlassian’s potential in 2024, balancing optimism with a realistic assessment of market challenges.

Long-Term Projections: What Lies Beyond 2024

When we look beyond the immediate future, the long-term projections for Atlassian Corporation Stock (TEAM) suggest a trajectory of growth and expansion. These projections, extending up to the year 2050, provide investors with a broader horizon for considering Atlassian’s potential as a long-term investment.

Yearly Forecasts up to 2050

Analysts have charted a course for Atlassian’s stock price, predicting significant growth in the coming decades. For instance, by 2025, the average price prediction stands at around $389.42, marking a considerable increase from the 2024 levels. This upward trend is expected to continue, with forecasts for 2030 suggesting an average price of $574.49.

Looking even further, predictions for 2040 and 2050 paint a picture of continued growth. By 2040, the stock is expected to reach an average price of $736.88, and by 2050, it could soar to around $2,004.04. These figures represent a substantial increase from current levels, underscoring the potential that analysts see in Atlassian.

Decoding the Growth Potential

This long-term growth trajectory is rooted in several factors. Atlassian’s commitment to innovation and its ability to adapt to changing market demands are key drivers of this potential. Moreover, the company’s strong foothold in the collaborative software market positions it well to capitalize on the growing demand for digital workplace solutions.

Investor Considerations for Long-Term Growth

For investors, these long-term projections offer a window into the potential return on investment that Atlassian could provide. While the tech industry is known for its volatility, Atlassian’s projected growth trajectory suggests a level of stability and potential for robust returns over time. However, it’s important to approach these projections with a degree of caution, as they are based on current market trends and assumptions that may evolve.

The long-term outlook for Atlassian is marked by optimistic growth projections, making it an interesting prospect for investors with a long-term investment horizon. These projections highlight the company’s potential to grow and expand well into the future, despite the ever-present uncertainties in the tech sector.

Investor Sentiments and Market Dynamics

Investor sentiment and market dynamics are crucial factors in understanding the stock market’s behavior, particularly for a company like Atlassian. These elements shed light on how investors perceive the company’s future prospects and how external factors might influence its stock performance.

Analyzing Investor Sentiment

Investor sentiment towards Atlassian has been generally positive, as evidenced by the modest level of short interest in its stock. A low short interest ratio suggests that a smaller proportion of investors are betting against the company’s success, indicating overall confidence in its future growth and stability. This positive sentiment is likely influenced by Atlassian’s consistent performance, innovative product line, and strategic market positioning.

Impact of Market Dynamics

The tech sector is known for its rapid pace and volatility, with market dynamics heavily influencing stock prices. Factors such as technological advancements, competitive pressures, regulatory changes, and economic conditions can all play a role in shaping Atlassian’s stock performance. As a leading player in the software industry, Atlassian’s ability to navigate these dynamics is key to maintaining investor confidence and stock value.

Investor Considerations

Investors considering Atlassian’s stock need to weigh these sentiments and dynamics carefully. While the current investor sentiment is favorable, it’s important to stay informed about changes in market dynamics that could impact the company’s performance. Keeping an eye on industry trends, competitor actions, and broader economic indicators will help investors make more informed decisions regarding their investment in Atlassian.

Investor sentiment and market dynamics are integral to understanding Atlassian’s stock performance. The current positive sentiment reflects confidence in the company’s future, but investors should remain vigilant about the ever-changing landscape of the tech sector and its potential impact on Atlassian’s stock.

FAQ

As of early 2024, Atlassian Corporation’s (TEAM) stock is trading at $237.00. This reflects the company’s market position and investor confidence at that time.

In 2024, analysts have given Atlassian Corporation a consensus rating of “Moderate Buy.” This rating is based on a comprehensive analysis by 19 analysts, considering various market factors and individual opinions.

Long-term projections for Atlassian’s stock show significant growth potential, with predictions reaching as high as an average price of $2,004.04 by 2050. These forecasts suggest a substantial increase over the years, reflecting analysts’ optimism about the company’s growth.

Investor sentiment towards Atlassian is generally positive, as indicated by the low short interest ratio. Market dynamics such as technological advancements, competition, and economic conditions also play a crucial role in shaping the stock’s performance. Investors are advised to consider these factors when making investment decisions.

Conclusion

Atlassian Corporation (TEAM) presents a compelling picture for investors in 2024. With a current stock price of $237.00 and a “Moderate Buy” consensus from analysts, the company demonstrates potential for growth amidst the dynamic tech sector. Long-term projections up to 2050 further highlight its promising future, indicating substantial stock value increases. Investor confidence, bolstered by positive sentiments and a keen navigation of market dynamics, positions Atlassian as a noteworthy consideration for those looking at long-term investment opportunities in the tech industry.

StockHax strives to provide unbiased and reliable information on cryptocurrency, finance, trading, and stocks. However, we cannot provide financial advice and urge users to do their own research and due diligence.

Read More