{kind=link}

This website and its content are not intended to provide professional or financial advice. The views expressed here are based solely on the writer’s opinion, research, and personal experience, and should not be taken as factual information. The author is not a financial advisor and lacks relevant certifications in that regard. We highly recommend consulting a qualified financial advisor before making any investment decisions, as the information presented on this site is general in nature and may not be tailored to individual needs or circumstances.

Stock trading online is often a very complicated proposition — after all, you’re trusting your investments to a company that will manage your funds over the Internet. You rely on their counsel and trust their judgment. Betterment and Vanguard are two of the more prominent stock traders on the market, but which one is better?

Contents

Features, Fees & Ratings Comparison Table

| Features | Betterment | Vanguard |

|---|---|---|

| 💰 Account Minimum | $0 | $0 |

| 💸 Commission Fees | 0.25% annual fee for digital plan, 0.40% for premium plan | $0 for online stock and ETF trades, $20 for mutual fund trades |

| 💼 Investment Options | ETFs, stocks, bonds, and mutual funds | ETFs, mutual funds, and stocks |

| 🤖 Robo-Advisor | Yes | Yes |

| 📊 Research and Analysis | Basic research and analysis tools | Extensive research and analysis tools |

| 📱 Mobile App | Yes, available on iOS and Android | Yes, available on iOS and Android |

| 🏦 Retirement Accounts | Traditional IRA, Roth IRA, SEP IRA, and 401(k) | Traditional IRA, Roth IRA, and 401(k) |

| 🎓 IRA Accounts | Yes | Yes |

| 📈 Trading Platform | No | No |

| 📞 Customer Service | Phone and email support available | Phone, email, and chat support available |

| 📚 Educational Resources | Basic educational resources | Extensive educational resources |

| 🌕 Fractional Shares | Yes | No |

| 🌱 Socially Responsible | Yes | Yes, through ESG funds |

| 🌎 International Investing | Yes (Foreign Stocks and Emerging Markets ETFs) | Yes (International Funds and ETFs) |

| 💳 Cash Management | Yes, through Cash Reserve | No |

| 🔍 Margin Trading | No | Yes, through Vanguard Brokerage |

| ⚙️ Options Trading | No | Yes, through Vanguard Brokerage |

| ₿ Cryptocurrency Trading | No | No |

| 🛡️ Account Security | SIPC insurance, two-factor authentication, and SSL encryption | SIPC insurance, two-factor authentication, and SSL encryption |

| 💹 Leverage | No | No |

| ⚖ Regulation | Regulated by SEC and FINRA in the US, FCA in the UK, and ASIC in AU | Regulated by SEC and FINRA in the US, FCA in the UK, and ASIC in AU |

Betterment vs. Vanguard: A Comprehensive Broker Comparison

Welcome to our comprehensive comparison of Betterment and Vanguard, two leading brokerage platforms in the world of investing. In this comparison, we will provide you with a detailed overview of each broker, their pros and cons, and a conclusion to help you decide which platform is the best fit for your investment needs.

Betterment

Betterment is a popular robo-advisor platform that offers a range of investment services, including goal-based investing, tax-efficient strategies, and low-cost, diversified portfolios. Founded in 2008, Betterment has quickly become a go-to choice for investors looking for a hassle-free, automated approach to investing.

- User-friendly interface

- Goal-based investing

- Tax-efficient strategies

- Low fees

- Limited investment options

- No direct indexing

Betterment is an excellent choice for investors who want a user-friendly platform, goal-based investing, and tax-efficient strategies. However, it may not be the best option for those seeking more diverse investment options or direct indexing. Its low fees and automated approach make it well-suited for beginner investors or those who prefer a hands-off approach to managing their investments.

Vanguard

Vanguard is a well-established investment management company, founded in 1975 by John C. Bogle. Known for its low-cost index funds and ETFs, Vanguard offers a wide variety of investment products and services, catering to both passive and active investors. Vanguard’s reputation for cost efficiency and long-term focus has made it a popular choice for many investors.

- Wide range of investment options

- Reputable company

- Low-cost index funds

- No account minimums

- Higher fees for small account balances

- Limited access to advanced trading tools

Vanguard is an excellent choice for investors seeking a wide range of low-cost investment options, including its renowned index funds. Its reputation for cost efficiency and long-term focus makes it a popular choice among both passive and active investors. However, it may not be the best fit for those with smaller account balances or those seeking advanced trading tools and research capabilities. Vanguard’s accessibility and diverse product offerings make it a solid choice for a broad range of investors.

Features & Primary Uses

One of the major differences between Betterment and Vanguard is the way they advise you on the best stocks to take. Betterment is fully automated, using software and algorithms to make recommendations for your investments based on what your goals and available funds might be.

Betterment’s automated online platform is a convenient and popular way for many investors to get simple, straightforward, hands-off trading done. For beginning investors, it’s hard to beat Betterment’s $0 account minimum, which makes it easy to get started without having to commit too much to the practice.

Most of the brokerage work is done through their desktop and mobile platforms, both of which are fairly streamlined and easy to use. Their mobile app, in particular, is very clean and user-friendly, giving even novice investors all the tools they need to understand and work with their accounts.

Vanguard, on the other hand, is a personal advisor service that offers real human brokers who will look over your portfolio and provide you with valuable assistance to get the most out of your investments. While there is still an automated element to the service, teams of advisors help guide each account as needed.

With its focus on human interaction and assisted brokerage, Vanguard’s service operates quite a bit differently than Betterment or other online brokerages. For instance, instead of just setting up an account, Vanguard recommends a consultation with a broker in order to solidify your trading goals before getting started.

The personal advisor service Vanguard offers requires a $50,000 minimum investment (if you invest $500,000, you get a dedicated advisor). After the consultation, the account is set up, and their advisor team monitors their client’s portfolio, updating the client on its progress and offering rebalancing as needed.

Rather than having to deal with everything yourself, as with online brokers such as Betterment, Vanguard’s personal service allows you to be more hands-off. If you need to consult your advisor, Vanguard has a toll-free number by which you can do that.

This personal advisor service is Vanguard’s chief point of difference from Betterment — while they have an online platform, it pales in comparison to Betterment’s functionality. In essence, choosing Vanguard involves you placing a great deal of faith in human investors to manage your accounts properly.

In lieu of human investors, Betterment allows users to set their own investment goals and allocation percentages. If you want to save for retirement, just set your desired savings goal and the date of your retirement, and Betterment will do the rest. Vanguard theoretically does the same, but instead a team of advisors are watching over your account so you don’t have to.

Investment Options

Both Betterment and Vanguard offer a bevy of options for investors of all stripes. On both services, you can set up taxable accounts (individual, joint and trust), as well as traditional, Roth, SEP and rollover IRAs. Vanguard offers mutual funds, as well, a service Betterment lacks.

They both also use the modern portfolio theory (MPT) to guide their investment strategy, which means a focus on diversified portfolios to maximize returns over a long period of time.

For Betterment, you can choose from a wide variety of ETFs with 12 different asset classes, giving you a tremendous amount of choice that you might not get elsewhere. What’s more, Betterment covers worldwide stocks, which is a much wider net than Vanguard (which only covers stocks in the US). Sure, Vanguard’s service is more specialized, but Betterment’s experience is more universal.

Fees

Some additional differences between Betterment and Vanguard come with their fees, which obviously vary given the different approaches each of them take toward brokerage.

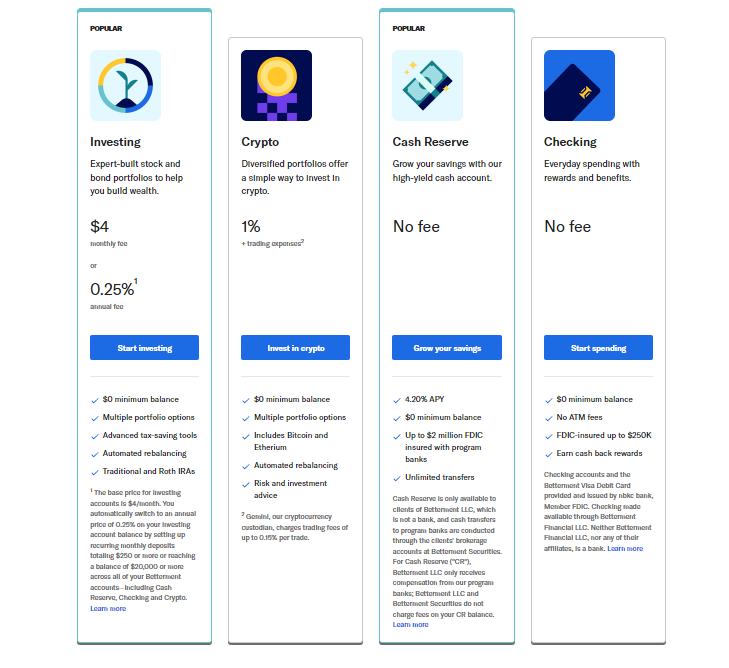

Betterment offers a three-tiered fee system, in which accounts of less than $10,000 offer a .35% fee, which lowers to .25% once you pass that threshold. If you have more than $100,000 in your account, however, that fee lowers even further to .15%, an industry low.

When it comes to account minimums, Betterment lets you have your account for free, which is advantageous for smaller or less experienced investors. This is a good deal more preferable than Vanguard’s $50,000 account minimum.

The no-minimum policy of Betterment means you can buy in at virtually any cost, and the tools provided are simple enough that you can just look on your app and make the essential decisions you need to get involved with your investments.

Advanced users, however, who want a bit more bang for their buck and are willing to get started at a higher level will likely have a lot to admire about Vanguard’s structured, personalized service.

Asset Allocation

When it comes to putting your assets in the right place to get the most money, the less automated service might work better for you. In this respect, choosing Vanguard would make a lot of sense — the teams of advisors assigned to your account would help you make educated decisions about your investments.

However, Betterment’s features are nice, as well. For instance, they offer automated tax-loss harvesting, which automatically sells some of your assets when it sees the potential for a tax-deductible loss, while purchasing those same stocks with other funds to keep your investment in line. This makes for tremendous earnings that require no human interaction.

For the most part, Betterment focuses on low-cost, liquid, index-tracing ETFs in order to give its customers the most bang for its buck. This gives investors the highest take-home returns possible, and lowers the annual cost of ownership quite a bit.

Vanguard, on the other hand, uses a series of portfolio allocation models to split investor funds between a preferred ratio of stocks to bonds. They have several to choose from based on what kind of investor you are — one who wants balance, one who seeks growth, or short-term income-based traders.

Which Should You Pick? Who Is Each Good For?

When it comes to picking between Betterment and Vanguard, the question is simple: Do you want convenient and cheap, yet automated, investment management? Or do you want to pay a little more for serious, personalized, human investment assistance?

Both of these practices have their pros and cons. Betterment is so incredibly easy to use, but you might not get quite as much out of your investments as you would with Vanguard.

From a customer service perspective, Vanguard is the better choice for those who need hands-on assistance with their investments. Having a real person on the line to assist you is an incredibly helpful thing, making Vanguard a little more personalized than Betterment’s automation.

At the same time, Vanguard’s service is great for people who have a little more knowledge about (and interest in) the stock market and their investments, or are at least willing to pay more to get people to watch over their investments for them. The comparative lack of streamlining and user-friendliness on Vanguard’s website pales in comparison to Betterment’s, so keep that in mind, as well.

That said, you may feel comfortable enough in your investment choices to work with Betterment’s high-quality online platform; even there, you get customer service in the form of phone support during office hours, as well as email and chat support.

In the end, Betterment and Vanguard alike will serve you perfectly well, regardless of your level of experience. Investors who feel more comfortable with a real broker by their side might want to side with Vanguard, but Betterment’s online solutions are extremely convenient and work for most people.

Conclusion

When deciding between Betterment and Vanguard, consider your investment goals, preferences, and experience level. Betterment is an excellent choice for investors who prefer a user-friendly platform with goal-based investing and automated tax-efficient strategies. It is especially suitable for beginners or those who want a hands-off approach to investing.

On the other hand, Vanguard offers a wider range of investment options, including its well-regarded low-cost index funds. It is a solid choice for investors who prefer more control over their investment selections and those who prioritize a reputable company with a long-standing focus on low costs and long-term investing.

Images by:

Rony Michaud, Nikolay F.

StockHax strives to provide unbiased and reliable information on cryptocurrency, finance, trading, and stocks. However, we cannot provide financial advice and urge users to do their own research and due diligence.

Read More