{kind=link}

This website and its content are not intended to provide professional or financial advice. The views expressed here are based solely on the writer’s opinion, research, and personal experience, and should not be taken as factual information. The author is not a financial advisor and lacks relevant certifications in that regard. We highly recommend consulting a qualified financial advisor before making any investment decisions, as the information presented on this site is general in nature and may not be tailored to individual needs or circumstances.

When it comes to choosing an online trading platform, it can be really difficult to pin down the specific differences between all the options out there. Betterment and Wealthfront are two of the biggest stock trading solutions, and we’ve compared them head-to-head to see which one is best for you.

Contents

Overview of Betterment & Wealthfront

| Features | Betterment | Wealthfront |

|---|---|---|

| 💰 Account Minimum | $0 | $500 |

| 💸 Commission Fees | 0.25% annual fee for digital investing; 0.40% annual fee for premium investing; no fees for cash accounts | 0.25% annual fee for investing and no fees for cash accounts |

| 💼 Investment Options | Stocks and bonds ETFs; cryptocurrencies through Coinbase | The investment options for Wealthfront include cryptocurrencies through Coinbase, not just stocks and bonds ETFs |

| 🤖 Robo-Advisor | Betterment offers a robo-advisor service that creates personalized portfolios based on your goals, risk tolerance, and time horizon | The robo-advisor service for Wealthfront is called Automated Investing, not Wealthfront Investing |

| 📊 Research and Analysis | Betterment offers a range of research tools, including market data, news, articles, calculators, and educational resources | Yes |

| 📱 Mobile App | Betterment offers a highly rated mobile app with features such as view and manage accounts, trade stocks and ETFs, deposit checks, transfer funds, and more | Yes |

| 🏦 Retirement Accounts | Betterment offers retirement accounts, including IRA, Roth IRA, SEP IRA, and 401(k) | Traditional IRA, Roth IRA, SEP IRA |

| 🎓 IRA Accounts | Betterment offers IRA accounts, including Traditional IRA, Roth IRA, and SEP IRA | Yes |

| 📈 Trading Platform | Betterment offers a web-based platform and a mobile app with features such as real-time quotes, watchlists, alerts, trade tickets, and more | Yes |

| 📞 Customer Service | Betterment offers phone and email support, as well as a help center with articles and FAQs | Phone, email, chat |

| 📚 Educational Resources | Betterment offers a range of educational resources, including webinars, podcasts, articles, videos, guides, and workshops | Yes |

| 🌕 Fractional Shares | Betterment offers fractional shares for stocks and ETFs | Yes |

| 🌱 Socially Responsible | Betterment offers a selection of socially responsible investments | Yes |

| 🌎 International Investing | Betterment allows international investing through ETFs that invest in foreign markets | No |

| 💳 Cash Management | Betterment offers cash management products that include Checking (which is offered by nbkc bank, Member FDIC) and Cash Reserve, a high-yield cash account | The cash management products for Wealthfront include Checking (which is offered by Green Dot Bank) and Cash Reserve (which is offered by multiple partner banks), not just Cash Reserve. |

| 🔍 Margin Trading | Betterment does not offer margin trading | No |

| ⚙️ Options Trading | Betterment does not offer options trading | No |

| ₿ Cryptocurrency Trading | Betterment does not offer cryptocurrency trading directly but allows users to link their Coinbase accounts to view their crypto balances | No |

| 🛡️ Account Security | Betterment offers two-factor authentication, biometric login, and account protection up to $500,000 through the Securities Investor Protection Corporation (SIPC) | 2FA, FDIC insurance |

| 💹 Leverage | Betterment does not offer leverage | No |

| ⚖ Regulation | Betterment is regulated by the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) | Registered Investment Advisor with the SEC and FINRA |

Betterment vs. Wealthfront: A Comprehensive Broker Comparison

Welcome to our comprehensive comparison of Betterment and Wealthfront, two leading robo-advisors in the world of investing. In this comparison, we will provide you with a detailed overview of each broker, their pros and cons, and a conclusion to help you decide which platform is the best fit for your investment needs.

Betterment

Betterment is a popular robo-advisor platform that offers a range of investment services, including goal-based investing, tax-efficient strategies, and low-cost, diversified portfolios. Founded in 2008, Betterment has quickly become a go-to choice for investors looking for a hassle-free, automated approach to investing.

- User-friendly interface

- Goal-based investing

- Tax-efficient strategies

- Low fees

- Limited investment options

- No direct indexing

Betterment is an excellent choice for investors who want a user-friendly platform, goal-based investing, and tax-efficient strategies. However, it may not be the best option for those seeking more diverse investment options or direct indexing. Its low fees and automated approach make it well-suited for beginner investors or those who prefer a hands-off approach to managing their investments.

Wealthfront

Wealthfront is another leading robo-advisor platform that provides automated investment management and financial planning services. Launched in 2011, Wealthfront has gained popularity among investors seeking low-cost, diversified portfolios, and a range of additional features, such as tax-loss harvesting and financial planning tools.

- Diverse investment options

- Direct indexing

- Tax-loss harvesting

- Financial planning tools

- Higher account minimum

- Limited human advice

Wealthfront is a great option for investors who desire a wider range of investment options, direct indexing, and financial planning tools. However, it may not be the best choice for those with a limited initial investment or who prefer more personalized human advice. Its focus on tax optimization and automated portfolio management makes it an attractive option for both beginner and experienced investors who prefer a hands-off approach.

Features & Primary Uses

Both Betterment and Wealthfront provide you with a basic, comprehensive online trading experience, and focus quite a bit on the budding trader. With either service, you can get tools and accounts that provide a lot of leeway for those people just now dipping their toes into the water.

Betterment is a New York-based financial advisor that currently manages $3 billion in assets, while Wealthfront is based out of Silicon Valley and manages $2.6 billion in assets. Both companies focus chiefly on offering competitive fees and commissions for investors.

Maybe Betterment’s best feature is that it offers a $0 minimum balance account, which has been one of its primary selling points for a long while. For those investors who wish to get their start with something simple, or who do not have a lot of money to invest, Betterment’s zero minimum balance is an extremely helpful incentive to begin (and more flexible than Wealthfront’s $500 minimum).

Since both are online investment platforms, the software is just as important a consideration as anything else. Betterment and Wealthfront alike provide proprietary software to help you create and manage diversified portfolios using certain criteria like risk tolerance, time horizons and age.

When it comes to the features on these programs, both companies offer services like tax-loss harvesting and automated portfolio rebalancing. However, Betterment differentiates itself by offering fractional share investing while Wealthfront provides single stock diversification, something Betterment lacks.

What’s more, Betterment provides investors saving for retirement with their RetireGuide, a program which automatically advises you how to save for your retirement. RetireGuide sets up a dynamic plan that is personalized to your goals, which is quite helpful. Wealthfront, by contrast, has no comparable system for retirement saving.

Investment Options

When it comes to helping you invest, Betterment and Wealthfront both work hard to create favorable systems to help investors of all experience levels with their goals.

Betterment provides financial planning, retirement planning, IRAs (Traditional, Roth, SEP and rollover), trusts and tax loss harvesting for its customers. What’s more, starting in Nevada, the company is starting to roll out 529 plans, making for a very comprehensive set of options for all kinds of investors.

Wealthfront offers a similar set of options, with non-retirement and retirement accounts of varying stripes. The overlap is extremely high, so it’s possible you’ll find whatever you need with either option.

Whatever your account type may be, Betterment and Wealthfront also offer similarly solid additional services to help you customize your account. Wealthfront, for example, gives direct indexing services for clients in order to optimize their investments and tax allocation.

Fees

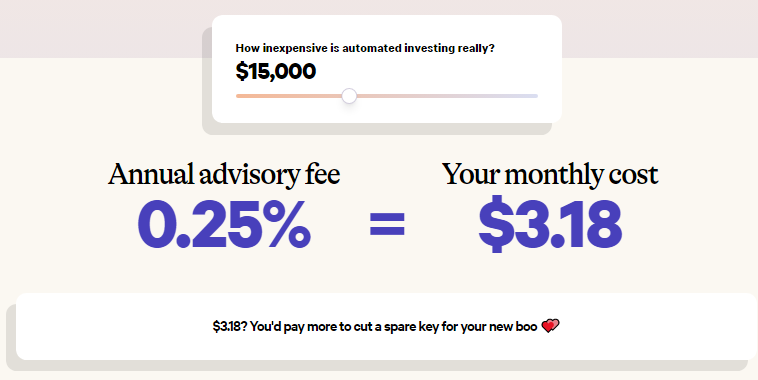

When it comes to fees, both Betterment and Wealthfront are perfectly good options for traders looking for an affordable platform in which to do their work. Betterment, for instance, has a very low fee structure, with .35% for the first $10,000, after which it goes to .25%.

Wealthfront, meanwhile, has an extremely low management fee system, with no fees for the first $10,000. Even after that, assets invested are charged just .25% as a flat advisory rate (the same as Betterment). Also, if you look around, you’ll be able to find promotional offers that can increase the no-fee ceiling to $15,000, particularly if you refer friends to the service.

When looking at both these companies in the simplest measures, Wealthfront’s flat rate is probably the simplest to understand. What’s more, the first $10,000 being free lowers the effective rate for investors at all levels, making it affordable even if you plan to invest big.

On the other hand, there is also a straightforwardness to Betterment’s three-tiered fee structure that is refreshing. If you have less than $100,000 in your account, you will end up paying more fees, but those with larger balances would benefit most from the .15% rate you get once you pass that threshold.

Asset Allocation

It’s one thing to offer a variety of accounts in which you can invest, but how do these services help you allocate assets to provide the best amount of diversification?

ETFs, in a nutshell, provide you with the ability to diversify holdings and limit your risk of losing money, while also making it easier to avoid high management fees that come with mutual funds that are more actively managed.

It’s here that Wealthfront outshines Betterment just a bit thanks to the high-quality resources they have to offer. Among their asset allocation features are differentiated asset location, daily tax loss harvesting, dividend reinvesting and automatic rebalancing of portfolios to account for risk tolerances.

In addition to that, Wealthfront just released a very impressive portfolio review tool, which all investors can check out for free.

Investments are checked for tax efficiency, cash drag, diversification and fees, giving investors all the tools they need to make informed decisions about their investments.

Betterment’s focus on investment, meanwhile, is on goal-setting, using the customer’s behavior and preferences to make recommendations on asset allocation. Account types are customized to certain goals that would work best for them, providing a great deal of flexibility.

One of Betterment’s more innovative tools is Smart Deposit, which strategically moves funds from your checking account as needed into your investments. It’s simple to set up – you just tell Betterment how much you need in your checking account for expenses, and if you go over that it deposits a bit into your Betterment account.

It appears as though Betterment has a much lower learning curve and greater sense of optimization and customization. More general investors might want to focus on Betterment, particularly people who are investing for a specific goal. Meanwhile, Wealthfront offers better savings for $100,000 or higher accounts with its tax optimization service.

Which Should You Pick? Who Is Each Good For?

While both Betterment and Wealthfront are generally good for traders of all stripes, they each have slight advantages in different fields.

Betterment is fantastic for traders who are attracted to the low fee structure, especially for higher-tier investors who plan to work with more than $100,000 in their accounts. Once you get to this point, you won’t find lower prices in the entire industry.

Wealthfront, by contrast, is much better for long-term passive traders who don’t plan to have very big balances in their accounts (the first $10,000 is always free to manage). That is, of course, unless you want to have more than $100,000 – then, Wealthfront’s tax optimizing feature can really pay off, perhaps a bit more than Betterment if used correctly.

What’s more, Betterment allows a great deal of flexibility with savings goals, and lets you set multiple to focus on simultaneously. Saving for short-term goals (a new car) and long-term goals (like your retirement) are completely within your reach with the same account, and Betterment can set up multiple goals to focus on based on their timing.

Both Betterment and Wealthfront offer wonderful incentives for smaller and more inexperienced traders, as they effectively have no fees for those not planning on throwing a fortune into their investment careers. If you want to start low, go with Wealthfront; but if you want to aim a bit higher, try Betterment.

In the end, however, go with whatever service feels right for you — both Betterment and Wealthfront provide somewhat comparable service, with the differences being fairly granular. No matter your choice, you are sure to get low fees, comprehensive customer service, and a variety of ways you can get your investment career started.

Conclusion

When deciding between Betterment and Wealthfront, consider your investment goals, preferences, and experience level. Betterment is an excellent choice for investors who prefer a user-friendly platform with goal-based investing and tax-efficient strategies, making it particularly suitable for beginners or those who want a hands-off approach to investing.

On the other hand, Wealthfront offers a wider range of investment options, including alternative investments and direct indexing for eligible investors. Additionally, its financial planning tools can be beneficial for investors with specific financial goals, such as retirement planning or college savings.

In conclusion, both Betterment and Wealthfront have their unique strengths and appeal to different types of investors. Consider your specific needs and investment goals when choosing the platform that is the best fit for you.

Images by:

©massonforstock/123RF Stock Photo, ©daviles/123RF Stock Photo

StockHax strives to provide unbiased and reliable information on cryptocurrency, finance, trading, and stocks. However, we cannot provide financial advice and urge users to do their own research and due diligence.

Read More